March was an awful month for U.S. equities as the S&P 500 Index fell almost 6%.

March was an awful month for U.S. equities as the S&P 500 Index fell almost 6%.

All sectors were negative except Energy (+3.9%) and Utilities (+0.3%), while the Magnificent 7 (“Mag 7”) sectors led the rout. Information Technology (Apple, Microsoft, NVIDIA), Communication Services (Alphabet, Meta), and Consumer Discretionary (Amazon, Tesla) all fell over 8% and were the three worst performing sectors. (1)

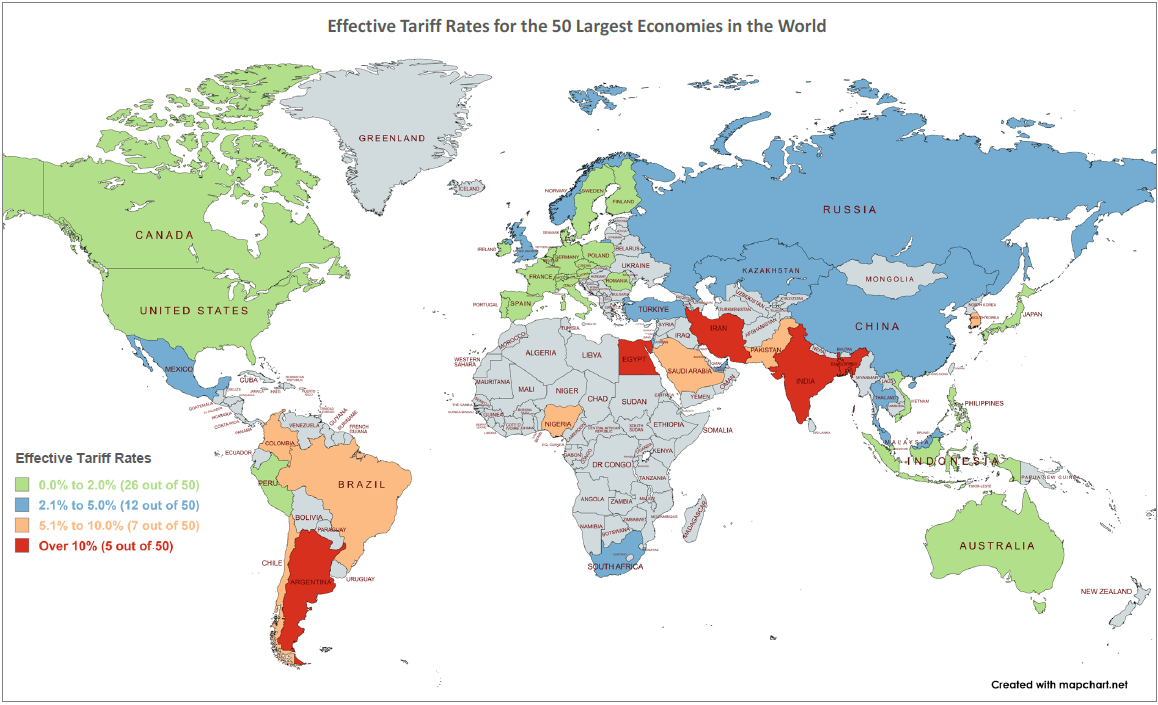

President Trump declared a national economic emergency on April 2nd as the basis for a slate of sweeping global tariffs including a baseline 10% tariff rate for all imports from any destination country (effective 4/5/25) and meaningfully higher tariffs (effective 4/9/25) for sixty of the “worst offenders,” including tariffs of 34% on China (on top of the 20% levy already announced), 20% on the European Union, 32% on Taiwan, 25% on South Korea, 46% on Vietnam, and 49% on Cambodia.

Trump’s “Liberation Day” initiative, which proposes significant tariffs on trillions of dollars in imports, signals a clear push from the White House to prioritize American-made goods for U.S. consumers. This marks a decisive shift away from the era of aggressive globalization that has driven the global economy for decades.

Q1 earnings season will begin in early to mid-April, with major companies like banks kicking things off. The forecast for the Q1 2025 corporate earnings season suggests a positive outlook, with total earnings for the S&P 500 expected to grow by 5.9% year-over-year, supported by a 3.9% increase in revenues. This follows robust growth in the previous quarter, and sectors like Aerospace, Consumer Discretionary, Medical, and Technology are anticipated to lead with double-digit earnings growth. (2)

The market returns on the 10-year Treasury yield jumped to 4.055% on April 3rd, around the levels seen in October, when it traded at 4.099%. Yields on the 10-year treasury bond are important because they are the benchmark for mortgage, credit card and other rates tied to economic growth. The 10-year crossed back above the 4% mark on Oct. 7; it has been hovering around the level and today’s move following “Liberation Day” decidedly puts it at the 4% handle. The trigger was due to risk-off stock selling and a flight to safe haven bonds. (3)

With the most recent Core PCE inflation data released on March 28, 2025, showing a year-over-year rate of 2.8% for February, inflation remains a critical indicator to watch closely as we assess the broader economic landscape and its implications moving forward. The core PCE inflation rate excludes volatile food and energy prices and is the preferred gauge of inflation by the Federal Reserve. (4)

With the most recent Core PCE inflation data released on March 28, 2025, showing a year-over-year rate of 2.8% for February, inflation remains a critical indicator to watch closely as we assess the broader economic landscape and its implications moving forward. The core PCE inflation rate excludes volatile food and energy prices and is the preferred gauge of inflation by the Federal Reserve. (4)

In this dynamic context, it is more important than ever for investors to have a clear understanding of the market’s state and the forces driving it. By staying informed and maintaining a balanced perspective, investors can make sound decisions that align with their financial goals.

As we roll toward the end of Trump’s first one hundred days, the full breath of tariffs will come into clear view as well as the health of corporate earnings. While I have often maintained that markets steer the economy rather than follow its lead, the interplay between the evolving tariff landscape and shifting consumer confidence could very well challenge this perspective—potentially redefining the dynamics at play.

As always, I will be here to provide insights into and analysis on the latest market trends and developments. Stay tuned for more updates in the next edition of “State of the Market.”

If you need to define whether you have any financial blind spots, please reach me directly at mark.martiak@prudential.com

1. Market Minute with Dave McGarel, CFA, CPA First Trust April 2025

2. Zacks.com

3. CNBC I MSN

4. CBS News I MSN

Mark Martiak is a Financial Advisor affiliated with LPL Financial and LPLe. Securities and advisory services are offered through LPL Financial, a registered investment advisor and member FINRA/SIPC. The views expressed in this column are solely those of the author and do not necessarily reflect the opinions of LPL Financial or LPLe. This material is for informational purposes only and is not intended to provide specific financial advice or recommendations for any individual.

Past performance is no guarantee of future results.

Such forward-looking statements are subject to significant business, economic and competitive uncertainties and actual results could be materially different. There are no guarantees associated with any forecast and the opinions stated here are subject to change at any time and are the opinion of the individual strategist. Data is taken from sources believed to be dependable, but no guarantee is given of its accuracy. Indexes are unmanaged, and investors are not able to invest directly in any index. Past performance is no guarantee of future results.

News items are based on reports from multiple commonly available international news sources (i.e., wire services) and are independently verified, when necessary, with secondary sources such as government agencies, corporate press releases, or trade organizations. All information is based on sources deemed dependable, but no warranty or guarantee is made as to its accuracy or completeness. Neither the information nor any opinion expressed herein constitutes a solicitation for the purchase or sale of any securities and should not be relied on as financial advice. Forecasts are based on current conditions, subject to change, and may not happen. U.S. Treasury securities are guaranteed by the federal government as to the principal and interest. The principal value of Treasury securities and other bonds fluctuates with market conditions. Bonds are subject to inflation, interest-rate, and credit risks. As interest rates rise, bond prices typically fall. A bond sold or redeemed prior to maturity may be subject to loss. Past performance is no guarantee of future results. All investing involves risk, including the potential loss of principal, and there can be no guarantee that any investment strategy will be successful.

The Dow Jones Industrial Average (DJIA) is a price-weighted index composed of thirty widely traded blue-chip U.S. common stocks. The S&P 500 is a market-cap weighted index composed of the common stocks of five hundred largest, publicly traded companies in leading industries of the U.S. economy. The NASDAQ Composite Index is a market-value weighted index of all common stocks listed on the NASDAQ stock exchange. The Russell 2000 is a market-cap weighted index composed of 2,000 U.S. small-cap common stocks. The Global Dow is an equally weighted index of 150 widely traded blue-chip common stocks worldwide. The U.S. Dollar Index is a geometrically weighted index of the value of the U.S. dollar relative to six foreign currencies. The market indexes listed are unmanaged and are not available for direct investment.

*The data and output from this tool do not constitute investment advice and is not a personal recommendation from CME Group. Nothing contained herein constitutes the solicitation of the purchase or sale of any futures or options. Any investment activities undertaken using this tool will be at the sole risk of the relevant investor. CME Group expressly disclaims all liability for the use or interpretation (whether by visitors or by others) of information contained herein. Decisions based on this information are the sole responsibility of the relevant investor.

Leave a Comment