As Americans gathered around the Thanksgiving table and recited what they were thankful for, market performance may have made the list. In a turbulent economic landscape, marked by a regional banking crisis, Middle East conflict, and a hawkish Fed policy, the journey has been anything but smooth. However, a series of positive developments has defied expectations, highlighting the surprising resilience of the US economy.

As Americans gathered around the Thanksgiving table and recited what they were thankful for, market performance may have made the list. In a turbulent economic landscape, marked by a regional banking crisis, Middle East conflict, and a hawkish Fed policy, the journey has been anything but smooth. However, a series of positive developments has defied expectations, highlighting the surprising resilience of the US economy.

Despite headwinds, including a regional banking crisis and geopolitical tensions, the economy has weathered the storm, thanks to a combination of factors. The Inflation Reduction Act’s new industrial fiscal policies, coupled with pandemic savings cushions and disinflation, have provided crucial support to housing prices and overall economic stability.

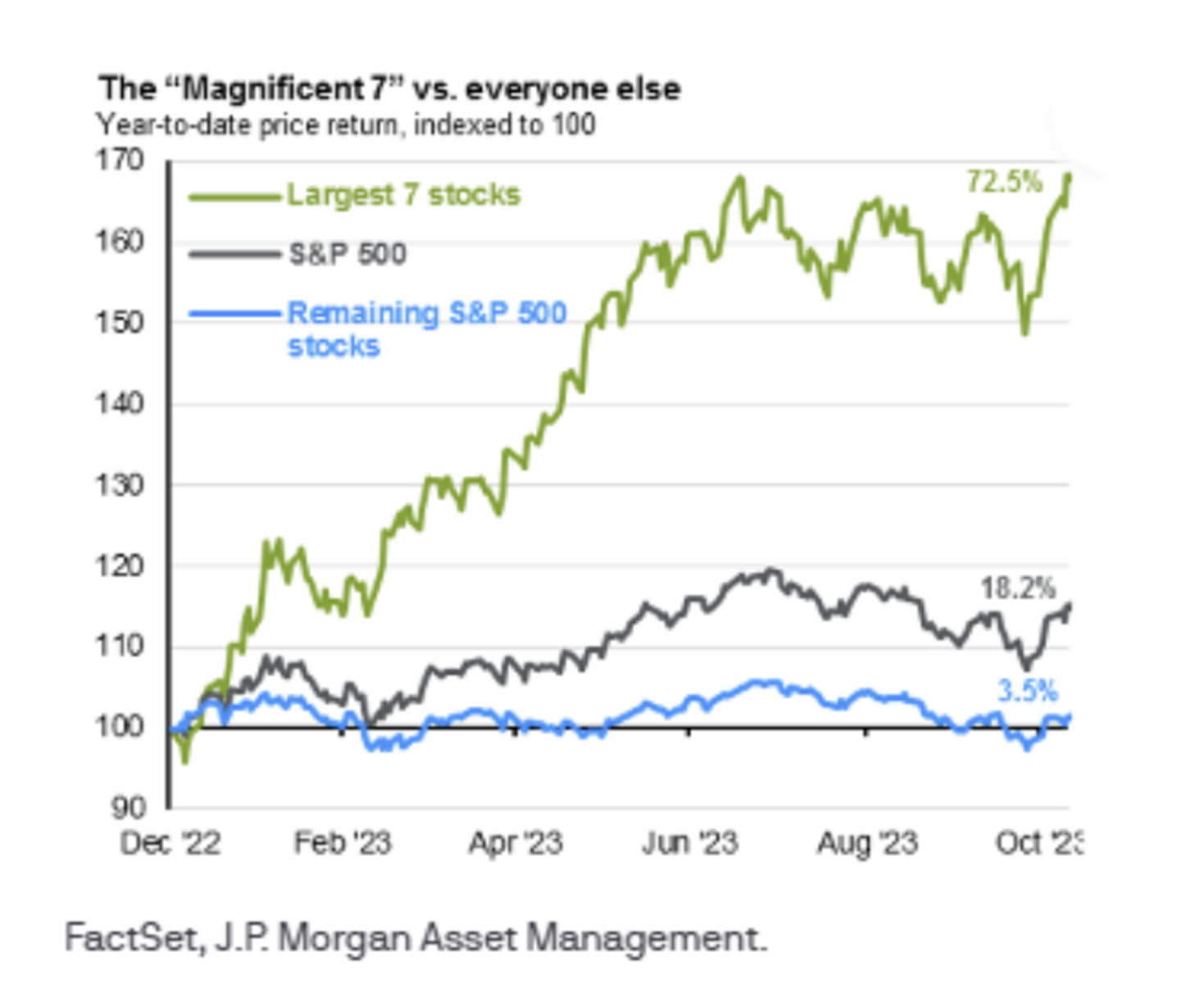

One of the most notable surprises has been the robust performance of U.S. large-cap growth, often referred to as the “Magnificent 7.” Remarkably, this group has surged by over 70% this year, contributing significantly to 94% of S&P 500 year-to-date returns.1This resilience is particularly striking against the backdrop of aggressive monetary tightening.

Moreover, the rapid integration of artificial intelligence (AI) into mainstream culture has played a pivotal role. Beyond sparking consumer excitement about AI sophistication, it has also sharpened investment focus. In the third quarter of 2023, more than 35% of S&P 500 companies referenced AI in earnings transcripts, signaling a growing emphasis on this transformative technology. Global private investment in AI is projected to soar to $200 billion by 2025, reflecting the widespread recognition of its potential impact on various industries.2

The Federal Open Market Committee left the target range for the federal funds rate unchanged at 5.25-5.50%. The post-meeting statement on November 1, 2023, was updated to acknowledge the recent tightening in financial conditions, a key reason for the pause. 3 With that, I interpreted Fed Chair Powell’s press conference as slightly dovish and continue to believe the FOMC has reached its terminal rate.

The Federal Open Market Committee left the target range for the federal funds rate unchanged at 5.25-5.50%. The post-meeting statement on November 1, 2023, was updated to acknowledge the recent tightening in financial conditions, a key reason for the pause. 3 With that, I interpreted Fed Chair Powell’s press conference as slightly dovish and continue to believe the FOMC has reached its terminal rate.

Treasury yields retreated from multi-year highs, easing what had been a major headwind to tech valuations. As I stated on Bloomberg.com November 9th: “I think we’ve seen a peak in Treasury yields, which will help with sentiment, especially for tech.”

I added that quarterly earnings results like Microsoft’s “suggest we’re past the worst, in terms of fundamentals,” and that “this combination of better fundamentals and a more favorable backdrop suggests tech can not only resume its leadership role but keep it over the rest of the year.”4.

For the fourth quarter of 2023, analysts are now projecting (year-over-year) earnings growth of only 3.2%. Do analysts believe (year-over-year) earnings growth rates will continue to decline sequentially into the first half of 2024?

The answer is no. For Q1 2024, analysts are predicting (year-over-year) earnings growth of 6.7%. For Q2 2024, analysts are projecting earnings growth of 10.5%. While these growth rates are below the expectations on September 30, they are still above the current growth rates for Q3 2023 and Q4 2023.5

In a series of eleven increases since March 2022, the Fed has taken up its key borrowing rate by 5.25 percentage points to reach its highest level in more than 22 years. Regardless, consumers, who power about two-thirds of the entire $26.8 trillion U.S. economy, have persevered.6

Expect the unexpected over the final month of 2023. The markets dictate the economy, not the other way around. Plan and stay disciplined about your asset allocation strategies. When you need to be defensive, cash can be your friend.

If you need to define whether you have any financial blind spots, please reach me directly at mmartiak@allianceg.com

Mark Martiak is a New York-based Investment Adviser Representative and Accredited Investment Fiduciary® for AGP / Alliance Global Partners, a registered investment adviser and broker-dealer, Member FINRA | SIPC. Mark is a regular Contributor to VEGAS LEGAL MAGAZINE and has appeared on CNBC’s CLOSING BELL, YAHOO! FINANCE MIDDAY MARKET MOVERS, FOX BUSINESS NETWORK and has been quoted in THE WALL STREET JOURNAL, Bloomberg.com and Investment News. Check out the Martiak Market Update Podcast wherever you listen to your podcasts.

Mark Martiak is a New York-based Investment Adviser Representative and Accredited Investment Fiduciary® for AGP / Alliance Global Partners, a registered investment adviser and broker-dealer, Member FINRA | SIPC. Mark is a regular Contributor to VEGAS LEGAL MAGAZINE and has appeared on CNBC’s CLOSING BELL, YAHOO! FINANCE MIDDAY MARKET MOVERS, FOX BUSINESS NETWORK and has been quoted in THE WALL STREET JOURNAL, Bloomberg.com and Investment News. Check out the Martiak Market Update Podcast wherever you listen to your podcasts.

Such forward-looking statements are subject to significant business, economic and competitive uncertainties and actual results could be materially different. There are no guarantees associated with any forecast and the opinions stated here are subject to change at any time and are the opinion of the individual strategist. Data is taken from sources believed to be dependable, but no guarantee is given of its accuracy. Indexes are unmanaged, and investors are not able to invest directly into any index. Past performance is no guarantee of future result.

News items are based on reports from multiple commonly available international news sources (i.e., wire services) and are independently verified, when necessary, with secondary sources such as government agencies, corporate press releases, or trade organizations. All information is based on sources deemed reliable, but no warranty or guarantee is made as to its accuracy or completeness. Neither the information nor any opinion expressed herein constitutes a solicitation for the purchase or sale of any securities and should not be relied on as financial advice. Forecasts are based on current conditions, subject to change, and may not happen. U.S. Treasury securities are guaranteed by the federal government as to the principal and interest. The principal value of Treasury securities and other bonds fluctuates with market conditions. Bonds are subject to inflation, interest-rate, and credit risks. As interest rates rise, bond prices typically fall. A bond sold or redeemed prior to maturity may be subject to loss. Past performance is no guarantee of future results. All investing involves risk, including the potential loss of principal, and there can be no guarantee that any investing strategy will be successful.

The Dow Jones Industrial Average (DJIA) is a price-weighted index composed of thirty widely traded blue-chip U.S. common stocks. The S&P 500 is a market-cap weighted index composed of the common stocks of five hundred largest, publicly traded companies in leading industries of the U.S. economy. The NASDAQ Composite Index is a market-value weighted index of all common stocks listed on the NASDAQ stock exchange. The Russell 2000 is a market-cap weighted index composed of 2,000 U.S. small-cap common stocks. The Global Dow is an equally weighted index of 150 widely traded blue-chip common stocks worldwide. The U.S. Dollar Index is a geometrically weighted index of the value of the U.S. dollar relative to six foreign currencies. The market indexes listed are unmanaged and are not available for direct investment.

1. FactSet, J.P. Morgan Asset Management Weekly Market Recap November 27, 2023

2. Goldman Sachs: AI investment forecast to approach $200 billion globally by 2025 published August 1, 2023

3. Press Release: Federal Reserve issues FOMC statement on November 1, 2023.

4. Bloomberg.com Technology: Microsoft Record Leads $1.5 Trillion Nasdaq Surge.

5. FACTSET: ANALYSTS EXPECT S&P 500 EARNINGS GROWTH TO IMPROVE IN 1ST HALF OF 2024 by John Butters November 10, 2023

6. CNBC: Retail sales increased 0.7% in July, better than expected as consumer spending is holding up; August 15, 2023

Leave a Comment